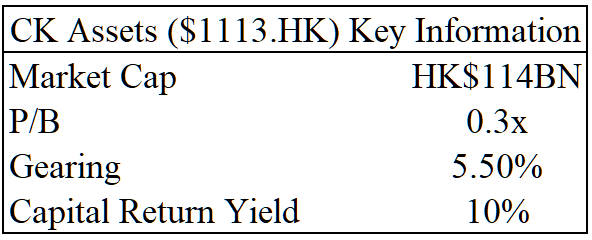

CK Assets

Misunderstood and mispriced

This is part of a series of posts on Hong Kong based property developers. For context on the sector as a whole, feel free to refer to Part 1.

If you bought Cheung Kong Holdings on IPO and held through all the corporate actions, you’d have an 8% CAGR: 12.5% CAGR 1972-2015; -8.5% from 2015-today. 12.5% isn’t quite Berkshire level, but it’s still super solid, and understanding the recent decade of underperformance is key to assessing whether the next decades performance will look more like the first or last decade. Pyramids and Pagodas had the same idea as me and we wrote it up at the same time, I’d highly recommend reading their post too. I think it covers the quantitative angle very well so I’ll focus more on the qualitative management angle here.

History

Cheung Kong Industries was founded in the 1950s by Li Ka-Shing to make plastic flowers and toys. Post-war Hong Kong was a major industrial export hub and saw living standards explode. In the 1960s he pivoted into real estate, listing his flagship Cheung Kong Holdings in 1972. Over the next few decades he expanded his empire globally into everything from retail (A.S. Watsons is the largest healthcare retailer in the world with 16k locations, vs 13k for WBA 0.00%↑ and 10k for $CVS); ports (Hutchinson ports is the 6th-largest port network by TEU throughput, and has been in the news recently as they operate the Panama Canal that President Trump complained about) ; infrastructure (everything from electricity to water, gas, rail and toll roads mainly in the UK and Australia); telecoms (one of the largest telecoms operators in Europe); and a whole litany of smaller segments like biotech.

Given that history, you won’t be surprised to learn the Cheung Kong family of companies is the most diverse and complex structure in HK. They’ve acquired more than US$200bn of companies - more than anyone else in HK. The most recent major restructuring was in 2015, when they merged the two flagship vehicles (Cheung Kong Holdings and Hutchinson Whompoa, a British trading house acquired in 1979) into CK Hutchinson ($0001.HK), and spun property assets into Cheung Kong Properties ($1113.HK).

Source: 2015 reorganisation investor presentation: Link

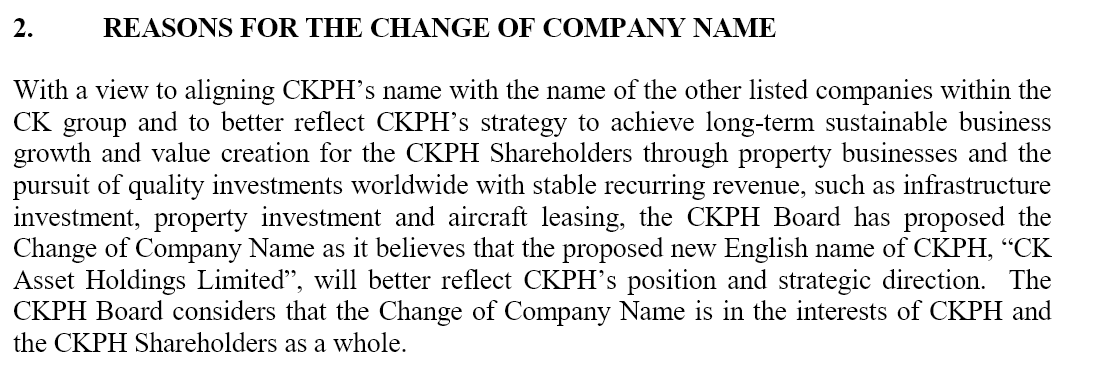

You can see above the rationale for the reorganisation - and I fully agree with all of them, especially ‘clear delineation between CKH Holdings (non-property businesses) and CK Property (a property play)’ . Bafflingly, two years later they decided that they would change the name from Cheung Kong Properties to Cheung Kong Assets for the reasons below:

Source: 2017 $1113 announcement: Link

They then did a series of public acquisitions and cross-purchases from other group companies, and today the structure looks like this:

At the time of the spin $1113’s revenues were 70/30 HK/mainland China. After 2017, they Their revenues are globally diversified, with broadly 1/3rd from Hong Kong, 1/3rd from the UK, 10% from mainland China and a quarter from the rest of the world.

But why did they restructure, then restructure again so quickly?

Now, these are unverified rumours, but it’s typically believed that Li Ka-Shing went to meet Xi Jin-Ping in 2012 when he came to power, as is tradition for the Hong Kong-based oligarchs. He waited in Beijing for days but was spurned, and after he left he pivoted his business away from China. China as a share of revenue dropped from 16.4% in 2011 to 7.4% in 2023.1 Practically all M&A were sales of investment properties in China to fund overseas assets, which didn’t go unnoticed. He was attacked by state media in 2015 with an op-ed titled “Don’t let Li Ka-Shing get away”; essentially calling him unpatriotic for divesting from China. CK had to release a public statement denying the allegations. In 2019, Li was again attacked by state media for being sympathetic to pro-democracy protestors by calling for ‘humanity’ in their treatment.

The point is Cheung Kong were very early to the realisation that the current Chinese administration weren’t as pro private business as previous leaders, and acted accordingly. I’ve covered this before in the primer, but in the good years developers in HK achieved 20-30% cash IRRs - far higher than what Cheung Kong gets from the more stable, recurring businesses across infrastructure, retail, pubs etc., where management’s target is double digit IRRs. If you’re looking to pivot away from China, while the HK/China business mostly in $1113 is throwing off these IRR numbers, it doesn’t take long before you need to shift cash from $1113 to $0001 through re-entering JVs. It’s also important to note that there’s a high probability Cheung Kong continues to diversify away from HK/China.

Do I agree with the pivot?

Philosophically, I disagree with the second pivot - much better to let investors pick the pure-play exposure to specific sectors they want, but I can understand the appeal to developers. Hong Kong development has just been so profitable that you don’t need excess risk (unlike the highly levered mainland developers) to get a decent return. The biggest problem is limited reinvestment scale - HK is ultimately a small city of 7m people where the high ROI is dependent on supply being less than demand, so developers ended up buying recurring income streams, typically investment properties held for rental income or in the case of Cheung Kong, globally diversified utilities/defensive consumer staples to cover the downside risk during crises. This way you print cash when the HK property market is booming, but aren’t at risk of going bust even through a protracted property downturn (like today).Were the related party transactions fair?

Ok, so it’s not the worst idea for CK Assets to go (back) into non-property businesses, but I’ve said lots of times that related party transactions are the favourite tool of these conglomerates to shift cash to the owners pockets at the expense of minorities. In the case of Cheung Kong, related party transactions are numerous but in my opinion, mostly fair.

The biggest recent one is acquiring partial stakes in 4 European utilities from the privately held Li Ka Shing Foundation in 2021. All of the infrastructure investments CKA owns are owned in JVs with Li Ka Shing personally, or CK Infrastructure (75% owned by CK Hutchinson), or Power Assets (36% owned by CK Infrastructure). The price was good, at 4.5x TTM weighted EBITDA which was significantly under market. It was paid with shares (that traded at a discount to NAV) so there was a bit of dilution there, but even factoring that in the deal was fair. Less than a year after the related party deal, PE tried to buy one of the assets UK Power Networks for ~£15bn (~HK$140bn). CKA’s 20% stake in UKPN would’ve been worth HK$28bn - HK$11bn more than the HK$17bn paid for all 4 stakes.

It’s not all perfect - in 2015 they tried to have Power Assets lend money to its parent company (voted down by minorities), a Pandoras Box for profit shifting, but there’s nothing ridiculous/deal-breaking.

Business Today

Again, Pyramids and Pagodas extensively covers the state of the business today and has a SOTP valuation I broadly agree with, so I won’t repeat too much here.

There are 4 segments:

Infrastructure, mostly in the UK/Europe/Australia making 7.5-8bn profit per annum attributable to CKA. These are defensive, regulated utilities with stable income. Public comps average 10x EV/EBITDA.

Investment properties for rent making 3-3.5bn profit per year. 80% of this is from HK. It’s an area they’ve been investing in with acquiring social housing in the UK and building a new flagship office building in HK (CKC II). This particular new building is pretty poor capital allocation as I outline in Part 1 of the series:

An example of what’s not so good would be Henderson Land (HK:12), who always lacked property in the CBD of Central, buying a plot of land at auction for US$3bn in 2017, redeveloping it into a flagship eponymous 190m-tall office building ‘THE HENDERSON’. Including build cost, it’s likely that they’re getting a <2.5% gross rental yield on the investment - hardly what you would call rational value maximisation. A year afterwards, in 2018, CK Assets (HK:1113) who lost in the auction announced they were redeveloping an existing 23 storey office next door to build CK Centre II, an office building 8 meters taller than the Henderson and positioned to perfectly block its prime harbour view. The building is finished, but a pitiful 10% of GFA has been leased. Again, shockingly petty behaviour that incinerated billions in shareholder value.

Property development for sale. This is the most cyclical but high ROIC part of the business. This is typically 50/50 HK/China with occasional negligible contribution from international markets. In 2023 CKA reported 13bn revenue from development and 4.5bn profit. This is down from 65bn revenue/21bn profit in 2019. For a reminder of HK development accounting quirks, review the primer.

A pub business making ~1bn profit. Margins are 1/3rd of pre-pandemic levels.

Random assets that won’t shift the needle too much, like hotels; property management (for previously sold developments); and a couple of listed REITs including 26% of Fortune REIT which I have previously written up here.

In a blue sky scenario where the property market swings back; the pubs go back to historical margins and infrastructure remains strong CKA could generate >40bn in underlying profit (excl. property revaluations) on a current market cap of ~115bn. In FY23 they made 17bn in profit - so it’s 6-7x trough earnings and <3x peak earnings.

Other key points to note are:

Every segment is profitable, including property development in Hong Kong and the Mainland despite the macro industry headwinds, due to the low leverage/slow development approach taken by management. Margins are fairly stable at ~33%.

There’s minimal leverage (6%) and a sizeable cash pile (HK$33bn, a quarter of market cap). There’s plenty of capacity to make big investments if distressed opportunities show up.

You can slice and dice the company in lots of ways but it’s cheap no matter how you look at it. You get international utilities at a discount because they’re stranded in HK, or you get a well-run property developer that’s dragged down because the broader Chinese real estate is going through a slow-motion implosion, or you get a Hong Kong property investor that’s trading cheaply because the office markets are a disaster, or it deserves a great big discount because it’s an unfocused conglomerate - pick whichever narrative suits you to explain the valuation and it still looks cheap afterwards. It’s been so conservatively run that it’s got minimal downside risk, has strong upside potential if management deploys capital appropriately at the trough and you get paid a mediocre 6% yield while you wait.

The phrasing I like to use is paying market rate for European infra (~80bn), + excess cash gets you to the market cap; and you get everything else for free.

Capital Allocation

The capital allocation of Cheung Kong over the past 60 years can be summed up as generating high ROIC profits from Hong Kong development, then redeploying capital outside its home market, with a marked shift out of China since 2012. This necessitates a huge amount of M&A, and the founder Li Ka-Shing has had an OK track record. There’ve been some misses and some hits, but on the whole there’ve been more hits than misses. It doesn’t compare to the returns in HK, but there’s a hard limit to scale there.

Going forward, the question is whether the capital allocation improves or gets worse as Li Ka-Shing steps down and his son Victor Li steps up. Officially, Victor became chairman of the Cheung Kong companies in 2018 when Li Ka-Shing stepped down to be ‘senior advisor’, but the reality is it’s been a long, long handover process. Victor was gradually given more capital to invest since joining in 1985; he became deputy chairman in 2015 and then chairman in 2018; but Li Ka-Shing retains an office in the headquarters and likely still has a say in the big decisions.

You’ll notice that the timeframe where Victor got more power broadly lines up with the period of underperformance I mentioned at the beginning. But I dont actually think this is entirely his fault. The market hated it when Cheung Kong focused on European investments over HK and China in (again, lower ROIC); and then the 2019 protests, Covid, and Chinese real estate bubble bursting have been one sucker punch after another. So they recognised the issues with China very early on and allocated well but got penalised by the market for it; then when the issues became apparent to everyone they weren’t rewarded by the market for that foresight and instead overwhelmingly penalised for their remaining exposure to China.

Assessing Victor’s capital allocation on a more fundamental level,

I like their newly discovered love for buybacks at these incredibly accretive levels; They return ~10%/year through dividends (6.5%) and buybacks (3.5%). Buybacks were never really used by Li Ka-Shing2 who favoured dividends (tax free in HK). Moving focus to buybacks should make the stock more appealing to international investors who don’t have the same tax treatment. The main issue if you’re looking for one is that they’ve been acquiring assets rather than really hammering those capital returns at these prices.

I don’t like his pub acquisition. CKA spent £4.6bn on 2700 Greene King pubs in 2019; and £485m on UK social housing REIT Civitas in 2023. The individual subsidiaries have also done smaller acquisitions which seem OK, but don’t really move the needle for CKA. Combined, they spent almost half of CKA’s current market cap on these two acquisitions; but they contributed just 1.3% of TTM profits. The acquisitions weren’t even overpriced, HK stock valuations are just that much lower. Management talks about M&A discipline and targeting double digit returns which is great, but even if they can achieve that the ROI on capital returns is just much much greater. I can understand the social housing acquisition. It’s property where CKA has great expertise; and the customer are councils who guarantee a stable, recurring income similar to their European regulated infrastructure investments. The pubs however have been a disaster with Covid restrictions and inflation pressures. They’ve managed to bring it back to profitability but operating margins (5%) are still way below the 15% peak that they bought it on. It doesn’t even fit with the strategic stable cash flow rationale of all their other European investments. Drinking might be the British national sport but spending on beer isn’t exactly mandated by the government!

Overall it’s probably too early to be judging Victor’s capital allocation, but that’s the main thing you need to monitor with CKA.

Conclusion

I think Cheung Kong are probably the best run large developers in Hong Kong. There’s a bit of worry about future capital allocation, but they’re cheap enough that I think it doesn’t matter, and it’s still a great buy. CK Hutchinson $0001 is also a very interesting situation where it’s almost entirely ex-China but still getting dragged down.

Revenue share is calculated across Hutchinson Whompoa and CK Holdings in 2011; and CK Hutchinson and CK Assets in 2023. CK Holdings doesn’t disclose 2011 geographical EBIT margins. My best guess is that China EBIT share dropped from 25% to <10%, as overseas assets are generally lower margin than property development.

Technically they did a few tiny buybacks, e.g. ~HK$500m in 2013, but it was <1% of Li Ka-Shing’s capital returns.

A great 👍 article, thanks!

What do you mean by:

"If you’re looking to pivot away from China, while the HK/China business mostly in $1113 is throwing off these IRR numbers, it doesn’t take long before you need to shift cash from $1113 to $0001 through re-entering JVs. " ?

Hi Praya, great writeup. I went through CK Assets financial statements, but can see only ~3b share of profit of JV (the utility assets) in IS and CF statements. I assume the 8b is not considering CK Assets' stake?