Transport International Holdings

6x the market cap the company does its best to hide from you

This is part of a series of posts on Hong Kong based property developers. For context on the sector as a whole, feel free to refer to Part 1.

Transport International Holdings ($0062.HK, HK$4.1bn market cap) operates 10,000 buses; owns 14% of Hong Kong’s stored value transport card; and a collection of properties. Both of the latter are hidden on screeners. A reasonable SOTP valuation would put the valuation at 6x the current stock price.

Transport

Hong Kong is one of very few cities that doesn’t have government-run public transport. Buses are regulated under a franchising system. Companies awarded a franchise can exclusively operate buses on a bundle of routes (designed to include both profitable and unprofitable but socially useful routes). The government regulates fares, bus frequency, service quality etc with a mandate to ensure ‘reasonable profitability’. This is defined as the ‘return on average net fixed assets over the trailing 10 years’ and ‘with reference to borrowing costs’. I.e. they target fare increases that allow for maintaining historic ROIC while keeping current costs in mind. In practice, there’s a ~1 year lag with government intervention so there’s a tendency for earnings to be cyclical or even negative in a worst case scenario. Over the business cycle, the transport segment has historically delivered ROIC-WACC of ~2-3%.

The transport business includes fully owned franchised bus companies in HK; fully owned unfranchised (i.e. private hire buses like tour/school) bus companies in HK; and bus/taxi/car rental JVs in the mainland. The franchised business makes up 95% of revenue.

Given the franchising system, there’s limited flexibility to optimise profitability for the operator. It’s pretty much a fixed-cost operation - it costs the same to drive a route, whether there’s 1 passenger on board or 100.

There are two big factors affecting profitability:

In normal times, the main variable is fuel cost - TIH doesn’t hedge fuel prices, so you can see an inverse relationship between fuel prices and profitability between 2013-19.

The load factor is typically fairly constant, as reflected by the daily rides/capita. This was heavily impacted by Covid and emigration through 2022, as Hong Kong had one of the most stringent and long lasting covid policies in the world. Today Covid is obviously over; and population is on an uptrend due to increased immigration from the mainland. I expect daily rides/capita to recover to a more average number of >0.37 this year which should increase underlying profitability.

I expect 2024 to deliver segment profitability around HKD$0.3/ride (or ~$300m). A normalised, average year delivers ~$450m in net profit. Critically, the government’s mandate for profitability is at the Kowloon Motor Bus operating subsidiary level, not the Transport International holding company level. The profitability of the property side doesn’t affect the requirement for the buses to be independently profitable.

The other transport businesses are lower quality due to the lack of barriers to entry, but they’re really too small to matter.

Octopus

The Octopus card was introduced in 1997 as a contactless stored value transport card. TIH was a founding member and owns 13.83 of the business, which today has developed into a leading electronic payment method in HK. 98% of the HK population uses the Octopus card, and it’s gone from being used just for transport to having >100k points of sales at convenience stores, restaurants, retailers etc. The business is extremely profitable due to the stored value (read: free float to reinvest) system, making ~HK$2bn revenue/HK$780m profit.

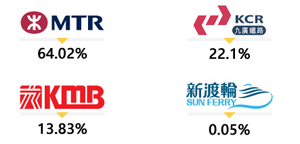

The company is private. Other shareholders are MTR ($66.HK); Kowloon-Canton Railway (operated by the MTR, but owned by the government); and Sun Ferry (owned by Chu Kong Shipping, $560.HK). KMB, or Kowloon Motor Bus, is TIH’s franchised bus subsidiary. IPO rumours float around every couple years, but there isn’t anything concrete.

It’s probably the most successful transport card in the world, but similar to other systems like Oyster in London, EZ-link in Singapore and Metrocard in New York, it’s seeing pressure from new payment methods. Hong Kong is especially intense as both Chinese methods like Wechat and Alipay; and Western methods like Visa/mastercard are competing.

The disclosures around this asset are extremely opaque. Ownership of Octopus isn’t even mentioned in any annual reports, and I’m not sure whether it’s accounted for as an ‘equity investment’ (which would technically be held for ‘trading purposes’ even though many HKEX companies hold these ‘trades’ for decades); as part of the KMB subsidiary segment (which is the wholly-owned entity that actually owns the stake) or somewhere else entirely. If anyone knows please comment below! The key is that this is a hidden asset that’s worth a much higher multiple than the transport or property segments. At 20x TIH’s stake would be worth >2bn, half their current market cap.

Properties

TIH owns a collection of real estate acquired in the 1960s/70s as bus depots. They are slowly redeveloping all of these in JVs with Sun Hung Kai (SHK, $0016.HK), TIH’s 43.83% shareholder.

Under HKFRS, properties held for investment (typically rented to 3rd parties) are held at ‘fair value’, i.e. they get appraised every year by an independent valuer and revaluation flows through the income statement. These valuations can be fairly ludicrous to be honest, as I highlight in my Hysan writeup. Often times they’re overvalued on very low cap rates; occasionally undervalued because management wants smooth, predictable revaluation gains. More interestingly, properties in use can be held at cost - accumulated depreciation. Actively used bus depots fall into this category and have all depreciated to insignificant book values; while the underlying land has skyrocketed in value.

Specifically they own:

5 run-down bus depots like the one below, 4 currently in use as depots and one converted to a logistics centre for HKTVMall ($1137.HK). These depots total >2m square feet. In the event of redevelopment, TIH will typically sell a stake to SHK; apply to rezone; and pay a land premium to increase the maximum floor area. The one below currently leased to HKTVMall has received rezoning permission. I expect redevelopment to happen after the market has recovered. This 105k sqft plot was held at $1.9m BV; and valued at $1.5bn (a cool 800x!) when half was sold to SHK. The other depots are similarly undervalued. It’s not often this type of asset comes up for sale so there aren’t a lot of recent comparables but conservatively the land bank is worth 15-20bn.

Importantly, there is nothing preventing redevelopment of the ones in use. They have previously redeveloped a bus depot to a residential/retail development and leased an alternative site from the government as a replacement. That series of transactions had a 30+% ROIC.

2 completed commercial buildings totalling 200k sqft. One of these is the retail section of the redevelopment mentioned in (1); and the other is TIH HQ, which uses ~10% of this. These generate a fairly steady profit of 50m HKD/year.

The Millenity

This is a mixed-use office(650k sqft)/retail(500k sqft) development in a 50/50 JV with Sun Hung Kai, Transport’s main shareholder. The lot was previously a bus depot. TIH sold 50% of the (industrial use) plot to SHK in 2006 for HK$490m. The JV then paid the government a further HK$4.3bn to rezone to office/retail, with a construction contract worth HK$4.4bn awarded to SHK’s construction subsidiary. Construction began in 2019 and finished in late 2022.

These related party transactions are often where these subsidiaries get shafted, but it doesn’t seem to have been bad in this case. The HK$490m sale was a tad low, but TIH would’ve had to take on a lot of leverage to fund it alone, and SHK’s expertise/reputation is worth quite a lot as well. The construction cost appears fair. I think the deal is a net positive for THI.

I touch upon the dynamics of the Hong Kong office and retail markets in my Hysan writeup which is useful context. The short version is: Macro environment is poor. The area is a Tier 2/3 industrial zone that has been slowly redeveloped into commercial - Grade A buildings like the Millenity saw strong demand tailwinds when the project obtained planning permission, but have seen strong headwinds after Covid.

In line with structural trends, as of our December site visit (2 years after completion), the office portion was 35% leased and the retail portion had not commenced pre-leasing. The retail portion has been delayed multiple times - first from 2023, to 2024, and most recently the timeline has been completely pulled. I do however think that by 2026/2027 leasing will improve. The Millenity is attractively priced at the same rent as 20-year old offices next door and most of their current tenants moved from nearby to this new build for ‘free’.

Assuming by then full occupancy at per sqft rent of HK$28/sqft (current actual achieved rents) for office and HK$80/sqft for retail (20% discount to going rate for the APM mall, a nearby mall also owned by SHK but with a direct connection to the MTR which typically commands a premium), you get a annual gross rental income of ~700m/ NOI of ~600m. The ~6% yield on the ~10bn cost is actually acceptable. If the HK property market hadn’t corrected, the yield on cost would be in the teens - very attractive for the HK market. Of course, this goes back to the comment on the sale price to SHK - the ‘fair market’ price to buy the plot would’ve been much higher, reducing the yield.

In short, by 2026/2027 I expect bottom line to structurally increase by ~300m/year due to the Millenity.

The retail not being leased out is a good demonstration of the related party issues that can happen. If TIH were independent, it’d make sense to lease out the Millenity even if you can’t fill it; but for Sun Hung Kai it’s better to fully lease out the wholly-owned APM than compete against yourself by opening the 72% (50% directly through JV, 22% pass through from TIH ownership) owned Millenity and impacting rental reversions at APM. The minorities get the short end of the stick.

Valuation

In total, you could see core earnings of $800m in 2026/27 (450 transport + 50 old commercial + 300 millenity), with the current MC at 4.1bn. The Octopus stake ~2bn isn’t included in this.

If we look at a SOTP:

Public transport businesses in Asia typically trade at ~7x normalised earnings = 2.8bn

If we capitalise $350m 2026 property earnings at a 8% cap = 4.4bn

Lower range of undeveloped land bank = 15bn

Octopus = 2bn

Total = 24.2bn

There’s also 1.5bn cash/4.5 debt. The vast majority of the debt is for the franchised bus segment and I’m lumping that implicitly into the 2.8bn segment value. I’m valuing that on a net income basis and not EBITDA because that’s what the government looks at when determining their allowed profitability, but if we value it on a EV/EBITDA basis and take out the net debt at corporate level, the ~1bn annual depreciation just cancels the debt out.

Conclusion

I mention in Part 1 of this series that the biggest factor in these microcap subsidiaries of large property developers is that you’re at the whim of these related parties - do you get a fair deal in the land acquisitions and JVs? Will the hidden land value ever be unlocked? Historically, the JVs have been at a pretty fair price, and they’re (veeeeery) slowly and steadily redeveloping the land bank. The catch is there’s no real catalyst for a re-rate - again the redevelopment is very slow, basically one project at a time over a decade; there isn’t really a possibility for an activist given shareholding structure; the controlling shareholder SHK isn’t likely to want to run the bus business and privatise TIH; and it’s <2% of SHK’s market cap so would hardly be worth their time anyway.

If those risks are acceptable, the sum of the parts is undoubtedly attractive , and SHK agrees - they have been buying more of TIH’s stock, going from 39.7% ownership in 2020 to 43.8%. Personally if I bought I would own it as part of a basket.

NOT INVESTMENT ADVICE

This content is for informational purposes only. You should not construe any information as legal, investment, financial or other advice. Do your own due diligence.

If you sum up all operational cash in flows for last 10 years, they barely cover all the capex outflow for last 10 years. At the same time, the debt has grown by 4.1B HK$ which looks like to be the main source of dividends. Makes me wonder if the company is actually making any money? Am I missing somenthing ?

Great write up- thank you! I was planning to look at them too but probably cant wait for a while, not sure what a catalyst here would be. That said ofc the bus depot for redevelopment is a great boon, had a good time with telephone exchanges being redeveloped back in the day, this seems similar, but again the question is how soon and is there a natural limit to doing 1 every X years coz SKH can only go so fast.