Hysan Development

Luxury retail/office exposure, will outperform on a market upswing.

This is part of a series of posts on Hong Kong based property developers. For context on the sector as a whole, feel free to refer to Part 1.

There’s an existing writeup from Guy Davis, but I think it’s worth writing a longer one that goes into more detail, especially around the (very real) risks.

Business Overview

Hysan is 42.17% owned by the Lee family (unrelated to the Lee family of Henderson Land (HK:12)). They got their start in 1920 when Hysan Lee received a monopoly to produce/sell/import/export opium in Macau - a license to print cash, giving him the nickname ‘the Opium King’. Hysan Lee was assassinated in 1928, but not before he bought a large plot of land in Causeway Bay (CWB) from Jardine Matheson (SI:J36) in 1924. The plot was originally supposed to be for an opium factory, but due to Hysan’s assassination and the mainland banning opium, this never materialised. Instead, the plot was used for everything from a theme park to a opera theatre, before gradually being developed into a prime mixed-use retail/office/residential district. Today, the company makes ~45% of its revenue from CWB office, ~45% from CWB retail, and the remainder from renting out an upmarket residential development in the Mid-Levels (popular with expats), and from stakes in prime retail assets in Shanghai.

Clean corporate structure

The problem I have with a lot of the Hong Kong family-owned real estate companies is the messy corporate structure. I highly recommend Joe Studwell’s excellent Asian Godfathers on the topic. Hysan is very simple - no privately held related parties or public subsidiaries.

Understanding prime HK Retail

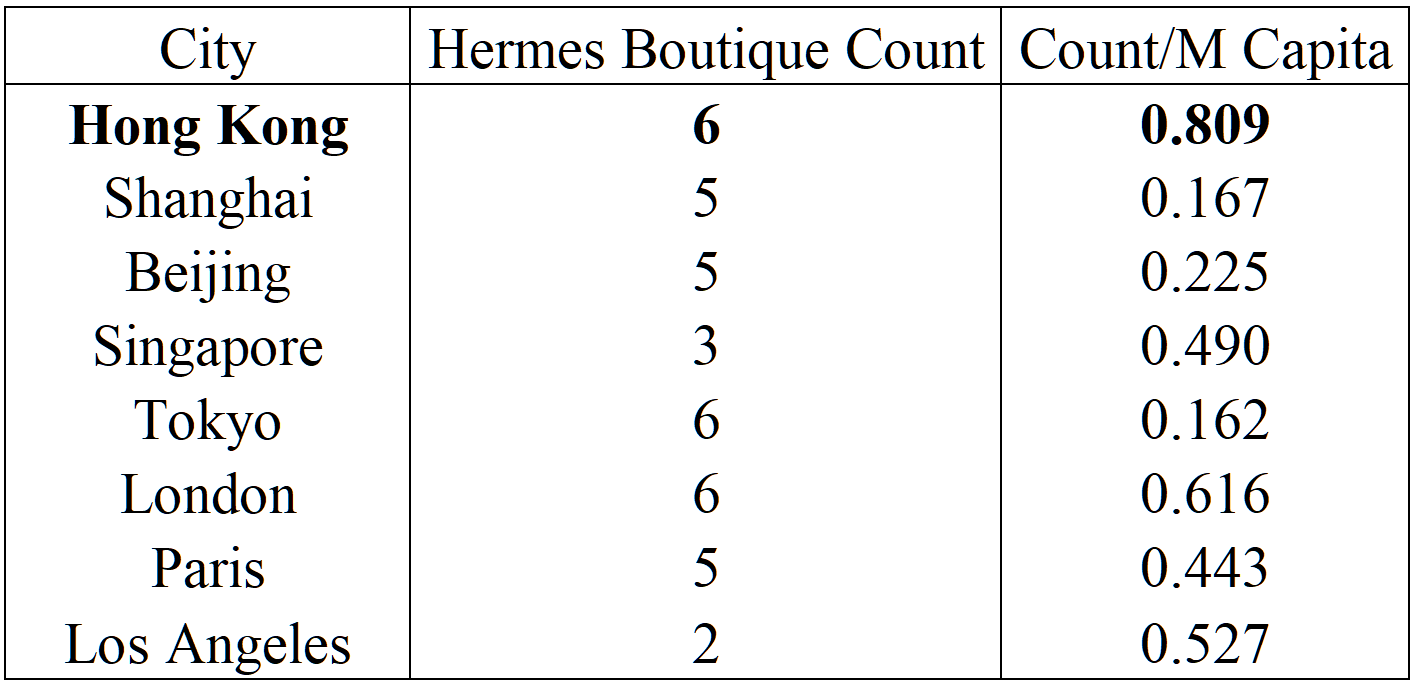

There are lots of different metrics to judge the quality of retail assets - rent/sqft, tenant revenue/sqft, cap rates, etc. At the peak of the Hong Kong real estate bubble, Russell Street in Causeway Bay used to be the most expensive shopping street in the world, ahead of 5th Avenue, Champs Elysées and Bond Street, but has seen rents fall by a third since then. The issue with these quantitative metrics is that they don’t capture ‘vibes’. Sheung Shui, another district in Hong Kong, used to have monthly rents at US$21/sqft - higher than somewhere like Kensington! But in reality, it’s a sleepy, rundown residential neighbourhood on the border with the mainland. The reason rents were sky-high is that there was huge demand for things like infant formula, which were perceived to be safer from Hong Kong after 8 babies were killed by mainland milk producers. People would come across the border, buy as many tins of formula as they could, and resell them in a grey market back home - hardly what you’d think of as a prime retail asset. Instead, the shorthand I prefer is to judge whether an area is top quality is to simply see if there’s an Hermes store in the area. They’re certainly competent enough to place their boutiques in the most exclusive areas in the world.

Globally, Hong Kong has the highest number of Hermes stores. Similar to the infant formula lower down the value chain, this used to be because Chinese tourists would come en masse to Hong Kong on holiday and buy luxury goods.

Hong Kong had:

No VAT/consumption/import tax (vs ~35% in the mainland)

A higher density of luxury brands

In recent years these advantages have eroded due to:

End purchase price harmonisation efforts by every major luxury brand

A strong HKD (pegged to USD) vs CNY

Another duty-free destination in Hainan, with simpler entry requirements than HK

Economic development in the mainland, with luxury brands entering Tier 2 cities.

Some of these factors, like currency, are transitory. Others are more permanent, and it’s likely that the heyday of Hong Kong as a luxury shopping destination is over. This has already partially happened through de-densification. In Causeway Bay for example, Louis Vuitton previously had two major boutiques - one with Hysan in Lee Gardens, and one in Wharf-owned Times Square, a mere 3 minutes walk apart. They have closed down the Times Square boutiqe and expanded the Lee Gardens one, with a net reduction in floor space. In my opinion, this de-densification isn’t enough. It’s likely that at least one of the luxury clusters will die out for the market to reach equilibrium. If this happens to be Hysan, it would be incredibly damaging - I expect the property value to go down by at least 1/3rd.

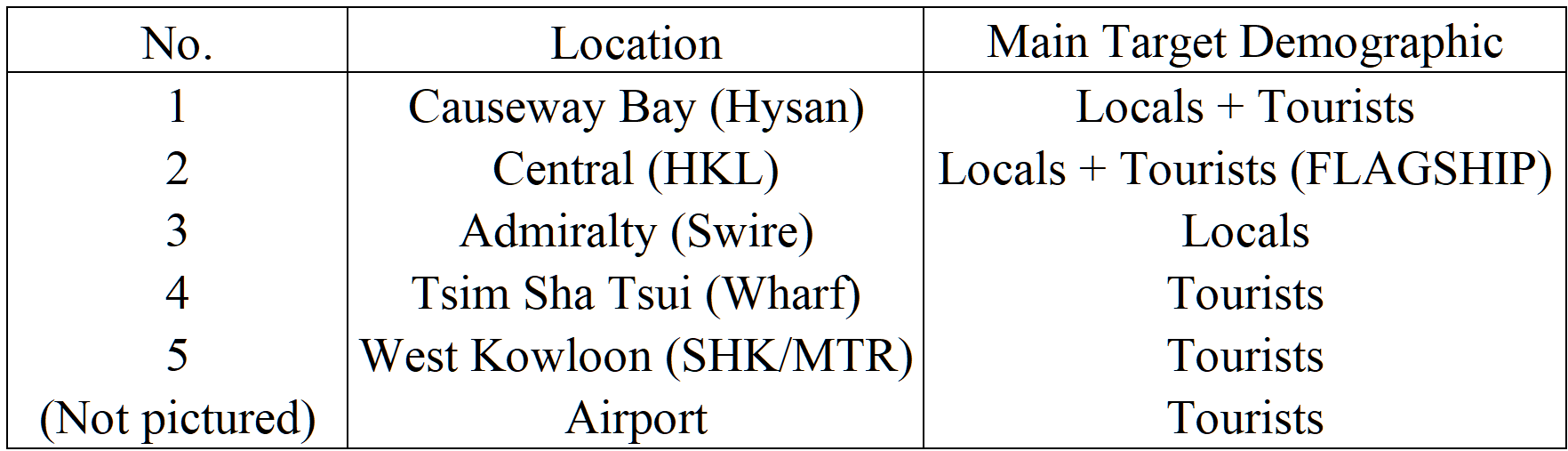

Looking at each cluster more specifically:

Causeway Bay is popular with both locals and tourists.

Central is the traditional CBD of Hong Kong, and most brands have their flagships here. This retail space is the highest quality in the city.

Admiralty is fairly weak. Geographically it’s close to Central, and typically viewed as slightly less premium by locals. It’s not touristy, and shops here are typically smaller in size - opposite of the larger experiential shops that are in vogue.

Tsim Sha Tsui is the most popular area for tourists to buy luxury items from. The shops in TST are the most productive (highest revenue/sqft) in the world for several brands. There’s been serious de-densification here, with brands pulling back from lower quality street-level locations into more premium malls like Wharf-owned Harbour City and New-World owned K11 Musea, but I don’t see the cluster going anywhere.

West Kowloon is fairly weak. The SHK/MTR JV-owned Elements mall is set under Hong Kong’s tallest building and is directly connected to the mainland by high-speed rail, but it’s geographically isolated, and tourists will pass at least one of the other clusters on their trips.

I expect either Admiralty or West Kowloon to gradually fade out over the next 5 years, depending on whether the local economy or mainland economy does better. Hysan in Causeway Bay isn’t the strongest (that would be Central, then Tsim Sha Tsui), but it’s far from the weakest either.

Understanding Prime HK Office

Central is by far the most prestigious location for offices in Hong Kong, to an even greater extent than it is for retail. Nowehere else is even remotely close. Irene Lee said at the last analyst meeting:

So when I sell to potential tenants, I'll challenge them, ask your staff, who wants to be here. It's very important, particularly now that people seem to have a choice to work at home. So I would like to make sure that your staff are happy. We always have the same thing. When Goldman Sachs came, when KPMG came, they don't dare bring their staff from somewhere else to come because they feel that they are disadvantaged because they want to be here.

I feel this is very misleading. A more accurate assessment would be that if you were to not work in Central, Lee Gardens would be a top choice - it’s geographically centered, the offices are nice, and there’s plenty of F&B/shopping options for leisure time. Generally speaking, being closer to Central is better - Admiralty, right next to Central, is a notch above the rest of HK Island; and being on HK Island (the lower half on the map above) is better than being in Kowloon (the upper half of the map above). The New Territories, which are even further north/ closer to the mainland are essentially suburbs.

And indeed, for many years the trend has been decentralisation (pun very much intended). Rents in Central are 30-50% higher than secondary locations, and became so unaffordable that even financial institutions and professional services were priced out of the market. Hysan, Swire (in Quarry Bay, further east of CWB) and other developers took advantage of this, building/updating offices to A-grade/ESG compliant levels. Many firms moved their back offices out of Central into areas like Causeway Bay, Taikoo Shing (Swire), parts of East Kowloon and so on from 2015-2018, with some moving their entire offices out of Central. For instance, Goldman leased 5 floors in Le Gardens for their back office while retaining an HQ in Central, while Baker Mckenzie moved their entire offices to Quarry Bay.

Since covid, the tide has shifted the other way. Firms are both downsizing (Goldman gave up a floor in Lee Gardens earlier this year) and eyeing the opportunity to move back into Central for the prestige now that rents are down 50% from the peak, and below what they were paying for these lesser locations a few years ago (Bytedance moved from Lee Gardens to Central in 2023). The focus on this ‘flight to quality’ has been on Central, but I believe that the same is happening further down the price ladder, particularly with mainland Chinese companies looking to use Hong Kong as a base for international expansion. These tenants would’ve previously looked for offices in lower quality areas like Kowloon Bay, but now have the opportunity to stake a spot on Hong Kong Island. Li Ning acquired a property on Hong Kong Island earlier this year, moving from Kowloon where their rival Anta is still located.

My view is that while the office environment is certainly tougher than it’s been for decades, and it’s unlikely to recover to previous heights unless US/China geopolitical tensions ease and bring more business to the anchor financial institutions, A grade offices located on Hong Kong Island will be fine. There’ll be transitory vacancies as the tide of decentrailsation has shifted, but it’s the A grade offices in Kowloon that will really struggle.

Understanding Hysan’s position in Causeway Bay

Competitors, how many sqft

Hysan is the largest commercial landlord in Causeway Bay, outlined with the red bounding box above at ~4.5m sqft. Other developers with a presence in area include Wharf ($0004.HK) with Times Square, Chinese Estates ($0127.HK) with Windsor House and Sogo, and Hang Lung ($0010.HK).

In 2021, they spent HK$19.8/US$2.6b in a 60/40 JV with ChinaChem, a private HK developer to acquire a plot of land on Caroline Hill at auction which will increase their GFA by ~1/5th. Market rumours suggested this was 35% higher than the closest bid. Including construction costs, total investment between the two partners is likely ~US$4.3b - in excess of the US$3.8b market cap of Hysan at the time (which is double the current market cap). At the time, management projected a 3% rental return and 25 year payback - ludicrously high numbers (but amazingly not the highest I’ve seen in HK). The property market subsequently collapsed and the rental return, assuming they get similar rates to what they’re charging in the rest of the portfolio, will be ~2.4%.

Source: Centaline Property Index, prices peak in late 2021

Management waxes lyrical about Caroline Hill being a strategic addition to the ‘community’ and the ‘strategic synergies’ to owning more GFA in a cluster, but the reality is it’s simply a massively overpaid mistake, and I expect this is something even management recognises in private. I think what they did afterwards is a lot more debateable, and useful for learning their thought process. In 2022, Hysan announced a US$250m ‘Lee Gardens Rejuvenation’ - major internal renovations, constructing footbridges to connect their various properties and so on. The idea was to follow the trend of ‘experiential’ shopping - fewer, larger flagship luxury stores; and more trendy pop-ups, community spaces etc to drive footfall. This was a significant undertaking for Hysan at a time when they were already spending significant capex on Caroline Hill; and the Hong Kong economy was in the depths of Covid with zero tourism. Whether you think this is a good idea is probably the biggest determinant of whether Hysan would be a good investment:

The bulls say:

The ability to invest at a market trough is exactly what keeping significant cash holdings in the good times are for.

You want to take out GFA for renovations when vacancies are high, rents are low at a market trough.

Hysan invests with a generational view, rather than a 3/5 year time horizon.

The bears say:

Hoarding cash to give you flexibility at the market bottom is value destructive over the economic cycle.

It’s foolhardy to spend so much money when the economy is in dire straits and the future of Hong Kong is uncertain.

This is egotistical empire building to have the nicest properties rather than rational investment.

Other businesses

Hysan has had a minority stake in Grand Gateway 66, a Shanghai office/retail complex; and full ownership of Bamboo Grove, an upscale Hong Kong residential development since before the millenium, but aside from that has been remarkably focused on their Causeway Bay portfolio. This is an undeniable attraction compared to many of the other HK developers that plow unending amounts of money into unrelated businesses while their core business trades massively under fair value. Obviously, neither is great but all else being equal, it’s probably better to destroy value in core assets (Caroline Hill) than unrelated businesses.

However, there are some worrying signs that they’re falling into the same trap as other conglomerates in recent years. In 2021, Hysan participated in the $US1.72b MBO of New Frontier Health ($NFH), a loss-making operator of private hospitals in China. The accounting is opaque but they spent ~HK$900m/US$120m, and fair value is likely down.

In addition, in 2021 they formed a JV with IWG to operate coworking spaces in the Greater Bay Area (Hong Kong, Macau and Guangdong). I don’t have much of a problem with this - it’s related to the core business; it didn’t require a big cash outflow; and it was a good hedge for if office culture changed permanently (which is looking less likely by the day).

Finally, also in 2021 (notice the trend?) they acquired a brand new office/retail complex from CK Assets in Shanghai for HK$3.8b, immediately renovating it and calling it ‘Lee Gardens Shanghai’. The development increased GFA by ~12%. Renovations have finally finished recently but given the state of the Chinese economy, pre-leasing is moving slowly. There’s also a plot of land next to the development, which Hysan might well bid for given the following commentary:

Lee Gardens Shanghai has strong value-add potential with commercial development opportunities with adjacent areas set out in the municipal government's master plan.

In essence, Hysan was conservatively levered and managed for decades, but in 2021, right before the Hong Kong real estate bubble burst, they made a series of large mistimed investments that have left them in a rather tough spot.

Valuation

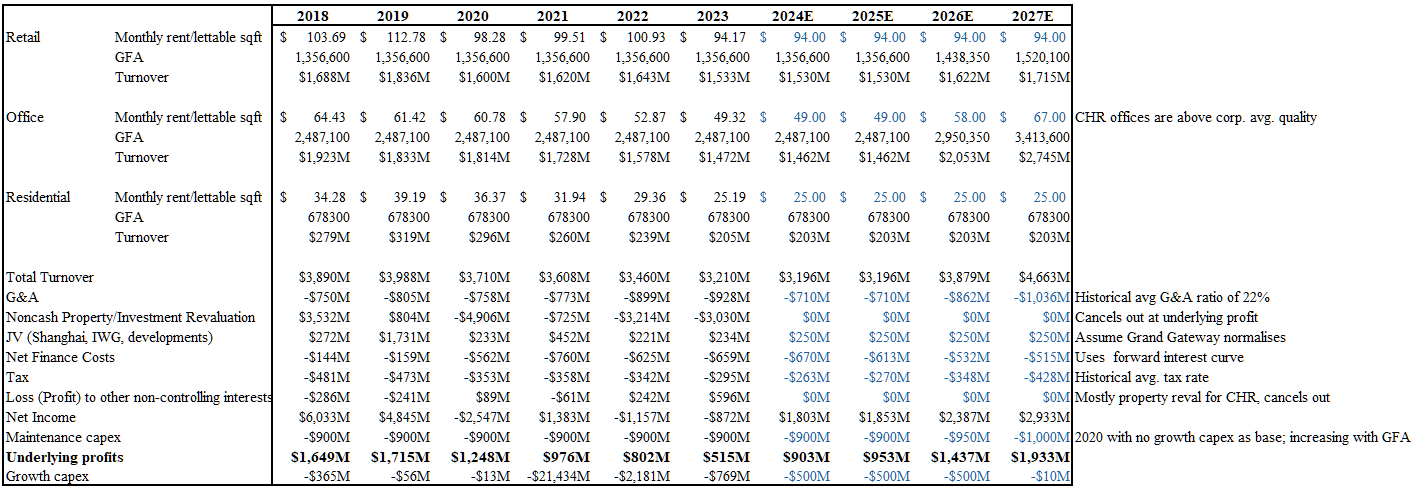

Officially, Hysan has a NAV of ~$65, and a discount to NAV of ~80%. However, I’m wary of using a NAV discount for a few reasons:

With completed properties in HK, there’s a significant difference in the ‘prevailing market rent’ used for appraisal and the actual rents realised, more than can be explained through rental reversions. If we use the actual rent and the same cap rates, the NAV discount shrinks to ~70%.

The appraisal capitalises gross rental income. This is arguably captured in the cap rate, but if you were to be more conservative and use net operating income instead and the same cap rates (property expense averages 22%), the NAV discount would further shrink to ~63%.

Caroline Hill Road is ‘valued’ at HK$19.19bn (as a reminder, they spent $19.78 on the land, implying they’ve lost ~3/4bn inclusive of build cost) - but if you look at the assumptions, the cap rate range for CHR of 3.5-5% is significantly lower than the 4.25-5% range historically used for Hysan developments literally across the road ; while the ‘prevailing market rent’ is lower than the rent from a decade ago. The cap rate range seems suspect here.

The (probably inflated given rents above in completed properties) assumed market rents are down 18% YoY, the cap rate range is ‘the same’ as FY22, but FV is somehow only down 2.3%. I’m not sure how Knight Frank justifies the hidden cap rate contraction given cap rates across HK office has only been rising, but either way, CHR is probably worth <15bn, or a ~10bn loss to Hysan in market value, or a ~68% NAV discount.

In general, with HK developers I’m not a fan of using NAV discounts if I don’t think there’s a chance of value realisation, and it doesn’t seem likely Hysan would break up their Causeway Bay empire which is the vast majority of value. I prefer to look at it from a cash/dividend perspective.

In my base case, HK property stays flat at this trough through 2027. By 2027, when Caroline Hill Road is finished, Hysan will produce ~$2bn HKD in underlying profit (which can be put into growth capex, debt principal payments or paid out), ~6.5x. In a more bullish case where rents revert to prepandemic numbers, it’s trading at ~4.5x 27E.

This seems fairly attractive - assuming that it’s properly deployed into debt repayment if interest rates are high/paid out. However, if they keep trying to expand, it’s a very different story.

Risks

The primary risk is that this ‘harvesting’ doesn’t last, and Hysan immediately goes on another redevelopment spree. They’ve already laid the groundwork for this. In Hong Kong, developers can apply for a compulsory auction if they own 80% of a property. This can be a decade-long process, and Hysan has acquired enough ownership of a collection of aging low-rise residential buildings backing onto their existing Leighton Centre and Lee Theatre, built in 1977 and 1994 respectively. They acquired these residential properties through 2020, before winning the Caroline Hill bid in 2021. It’s pretty clear that ‘Plan B’ if they didn’t win the bid was to consolidate the entire area into a mega development, rivalling Times Square across the road. The reasonable, value-maximising thing to do with these assets now would be nothing, but given management’s oft-quoted love of the ‘long term view’ and ethereal concepts like ‘community’, in my opinion it is a very real possibility that after shortly after Caroline Hill is finished, they go ahead with redeveloping this area.

Conclusion

The upside and downside are fairly defined. It’s cheap if you think management will do as they say and harvest, and expensive if you think they will do what they’ve historically done and build, build, build.

Management philosophy is very divisive. You either like the way they think about things on a decades-long basis, or you don’t.

NOT INVESTMENT ADVICE

This content is for informational purposes only. You should not construe any information as legal, investment, financial or other advice. Do your own due diligence.

Irene Lee is an ex-banker, probably gets new calls weekly about potential deals. Not great. By the way, another reason why Hainan is winning is that the cap for duty free is CNY 100,000 vs CNY 12,000 in Hong Kong.

Thanks for this write up. How cheap and how expensive could maybe be defined in more detail